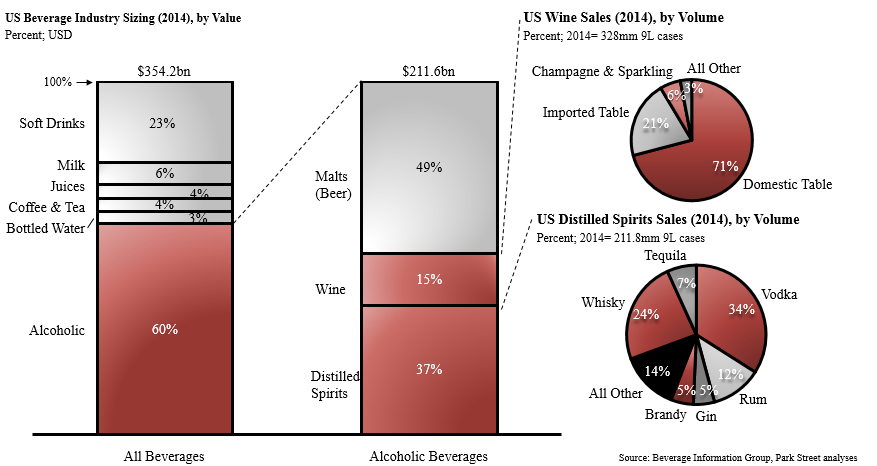

The U.S. beverage market is a $354.2bn industry with alcoholic beverages making 60% of the revenues with $211.6bn in sales. The alcoholic beverage market is almost equally split between malt beverages on the one hand and wine and spirits products on the other hand. Distilled spirits make up around 37% of the sales of alcoholic beverages. The largest sub-category of spirits is vodka with 34% of cases sold, followed by whiskey with 24% and rum with 12%. Wines make up around 15% of the alcoholic beverage market. 71% of the cases sold are domestically produced wines and 21% are imported wines. Champagnes and sparkling wines make up around 6% of the wine volume.

US Market Universe of Wine and Spirits

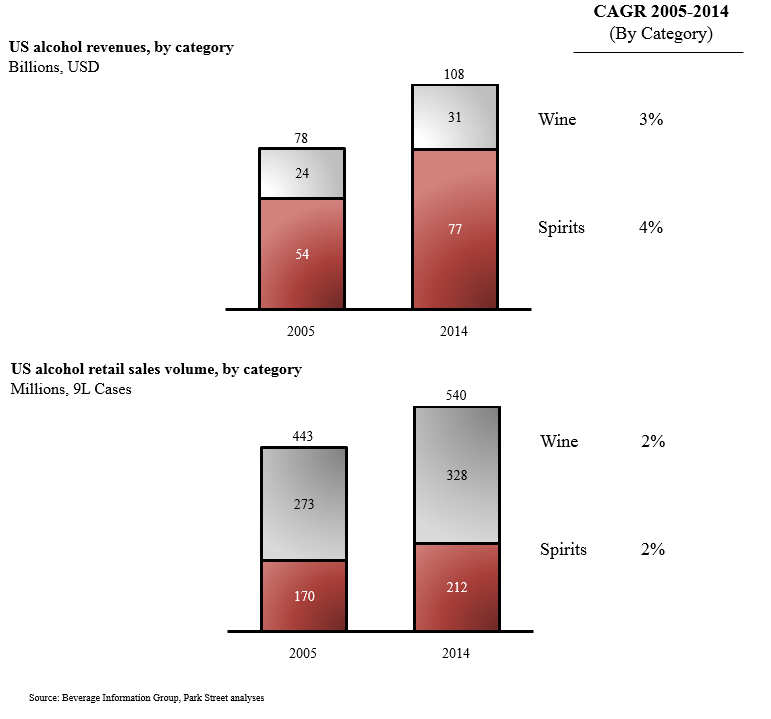

Industry has been growing with revenue outpacing volume on the spirits side

The wine and spirits industry has experienced steady growth over the last ten years. The spirits segment volume has been growing at a CAGR of 2% over the last 10 years while revenues outpace this growth with a CAGR of 4%. The wine segment has been growing steadily at a CAGR of 2% over the last ten years in volume and a CAGR of 3% in revenues.

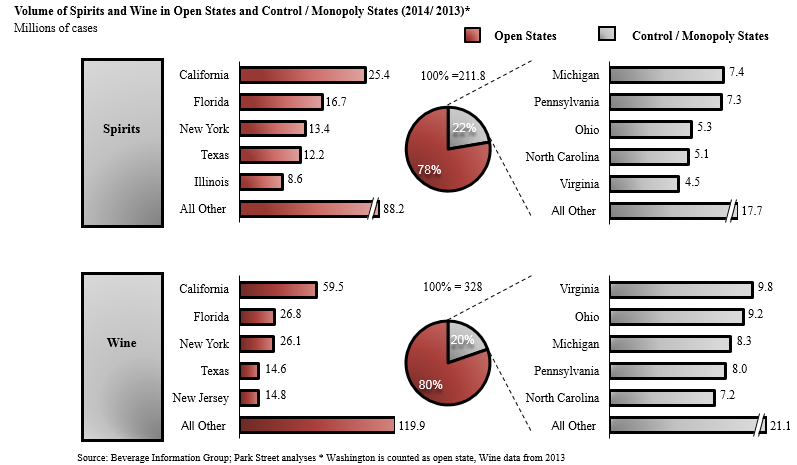

Open States are approximately 80% of the volume for both wine and spirits

Around 80% of the volume in the US is sold into open states while around 20% are sold into control/monopoly states. The largest markets are California, Florida and New York.

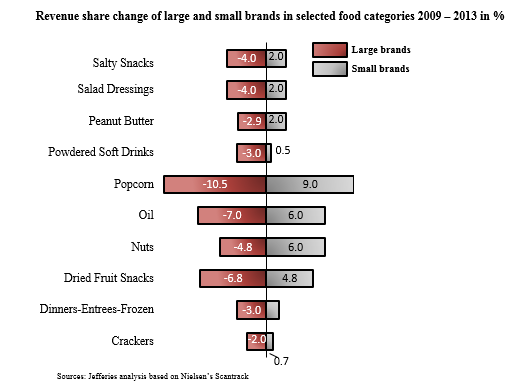

Revenue share change of large and small brands in selected food categories 2009-2013 in %

Smaller brands taking share of larger brands is a phenomenon across many FMCG (fast moving consumer goods) categories. Factors often cited as reasons include: shortening life cycles of brands in general, entrepreneurial innovation wave, liberalization and de-concentration of marketing avenues (e.g., Internet), premiumization, desire of consumers to differentiate themselves.

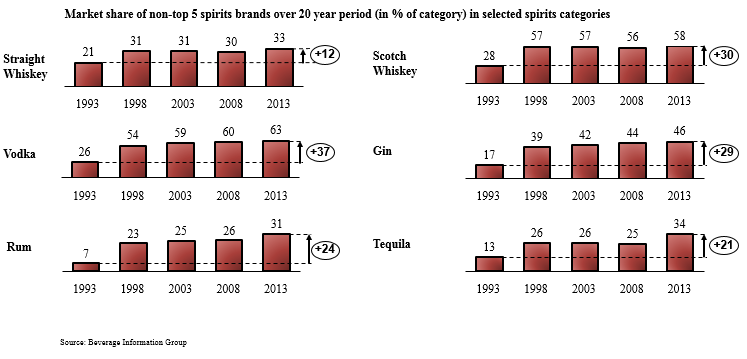

Market is getting more fragmented- smaller brands have been gaining share

Smaller brands have been gaining share. The non-top 5 brands gained between 12 and 37 percentage points over a 20 year period and between 2 and 9 percentage points in the last 5 years.

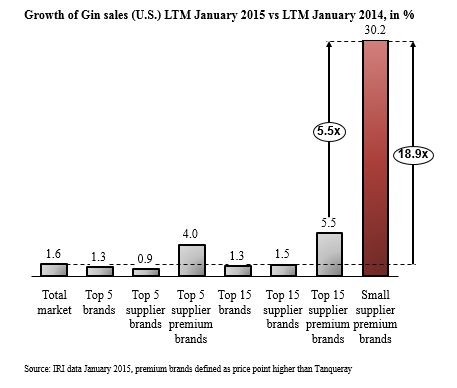

Smaller brands growing fast- example gin category

Small premium brands outgrew large supplier premium brands by a factor of 5.5x and the overall market by 18.9x. Approximately 45% of the category growth is coming from small supplier brands. This is remarkable, especially given that the account selection (e.g., no on-premise) and data availability typically provides a bias towards national and larger brands.

For more information, visit: http://www.parkstreet.com/alcoholic-beverage-market-overview/

{kind=link}